The Heron Partnership utilises a holistic methodology to assess and rate the various components of a superannuation fund, grouped under 5 Areas of Importance. The assessment covers about 150 features under these Areas of Importance, which are:

| Area of Importance | Standard Weighting % |

|---|---|

| Investment Arrangements | 55 |

| Insurance | 30 |

| Ancillary Benefits | 5 |

| Communications | 5 |

| Contributions | 5 |

| Total | 100 |

The primary goal with our rating process is to provide a realistic and objective representation of product strengths and weaknesses. Ratings are only performed at an Area of Importance level and are based on feature specific benchmarks which guide our assessors to rate the feature objectively. The ratings for each feature are aggregated to an overall rating for each Area of Importance.

The 5 Areas of Importance we assess cover the key aspects of the operation of a superannuation fund.

We undertake an assessment of the overall investment arrangements of each product and capability of each service provider, based on the following key criteria:

| Key Criteria | Weighting % |

|---|---|

| Multi-Manager Options | 20 |

| Default Options | 10 |

| Alternative Managers | 7 |

| People | 27.5 |

| Performance | 27.5 |

| Transaction Related Issues | 8 |

| Total | 100 |

Each Key Criteria represents an area that is analysed and is scored out of a possible maximum score of 10. The weighting for each Key Criteria is then applied to the score out of 10 and aggregated to show a total score out of a maximum of 10.

1. Multi-manager options - a high rating here would suggest a good range of diversified and sector multi-manager options covering all the common portfolios. To score highly the range should include a well constructed set of portfolios without a bias to the "house".

2. Default Options - a high rating here reflects flexibility in the range of default options possible. Where default options available have a bias to the "house" the rating is reduced.

3. Alternative Managers - a good range of alternative managers has the advantage of satisfying members requiring a wider choice when perhaps the sponsor or blended options are not performing well. A wider range of alternative managers is therefore not so necessary when the provider has pure multi-manager options.

4. People - this is a key determinant of investment performance in the multi-manager portfolios. A high rating reflects a dedicated team or investment sub-committee/CIO is in place, there is access to good external research, through a well credentialed asset consultant, providing strategic advice and ongoing monitoring.

5. Performance - is important for the multi-manager portfolios, particularly from the member's perspective as these are often the high profile flagship numbers freely available in the press and publications. Performance should be strong and consistent across the key portfolios e.g. balanced, balanced/growth and growth, as these are the popular portfolios used by members seeking active investment management.

Investment performance has been analysed across each products multi-manager suite of options, which are the most popular options selected by fund members. This allows Heron to establish a common ground for comparing different investment products. Heron have reviewed three different risk profiles: growth, balanced growth and balanced for scoring purposes.

The portfolios are classified by their strategic asset weighting to growth versus defensive asset classes. Growth assets include Australian and Overseas Shares, Property (listed and unlisted) and other miscellaneous equities such as infrastructure and private equity investments.

We have classified the growth multi-manager options as those with 80% - 90% invested in growth assets and between 10% - 20% invested in defensive assets.

We have classified the balanced growth multi-manager options as those with between 65% - 80% or more invested in growth assets and between 20% - 35% invested in debt assets.

The Balanced Growth portfolio is one of the most important portfolios because this is the one that most members are likely to be exposed to over their superannuation savings history and the one that is often selected as the default risk/return choice of members and for defined benefit portfolios in corporate funds.

We have classified the balanced multi-manager options as those with between 45% - 65% or more invested in growth assets and between 35% - 55% invested in debt assets.

This is an attractive portfolio for the more conservative long term investor and mature, closed defined benefit funds.

6. Transaction Related Issues - a high buy/sell cost and switching fees are costs to members who move portfolios. There are also costs incurred when considering a move to another provider. Frequency and methodology of unit pricing is also considered with daily forward unit pricing being the standard requirement for compliance, efficiency and equity. Timing of effecting switches is also considered.

Most superannuation products offer insurance. There is a great variance in the types of cover that are offered. These can include death only, death and Total and Permanent Disablement (TPD), and salary continuance type of benefits. Within each of these benefit types there are also many variables. Our assessment considers the number of options and hence the flexibility of the insurance offering.

In particular, we consider things such as eligibility conditions, definitions for TPD and salary continuance, exclusions, Automatic Acceptance Limits, waiting period options for salary continuance, free cover periods, and many other features. We identify the underlying insurers and also have regard to their Standard and Poors rating.

Overall, we place a heavy emphasis on the depth and flexibility of the insurance arrangements and hence give it a 30% weighting within our overall rating.

Many superannuation products are able to negotiate and offer non superannuation benefits to members and their families. Although not critical to the core product a member is selecting, it is useful to be familiar with those products that do have some other services that can be used as an advantage to the member. A high rating in this Area of Importance reflects many ancillary type services being available, which may include discounted housing loans, discounted (non superannuation) investment options, discounted travel, shopping services, spouse benefits etc. A low score indicates that there are few ancillary services available.

We weight the ancillary services as only 5% of the overall score.

The communication events that occur are important to fund members. The easy access to information through the web or the call centre is also important. A high score for communications will indicate that communication is done on a frequent basis with mail outs and other information being readily available.

Overall, this Area of Importance has a weighting of 5% to the total score.

The corporate market will generally allow a fund to accept any type of contribution (subject to regulatory restrictions). However, more so in the retail personal superannuation market certain restrictions are placed on the contributions that can be accepted into the fund. Those with minimal restrictions will score well. Those that require minimum contributions or who are unable to accept certain types of contributions (salary sacrifice, or employer additional contributions, etc) are penalised.

This Area of Importance has a 5% weighting to the total score.

Although overall cost is a critical component that needs to be taken into account in selecting a superannuation fund it is not one of the Areas of Importance that we separately rate. Our ratings reflect our assessment of the "quality" of product.

Because of the importance of fees, we treat it separately. There are a number of fees and charges that impact the operation of a superannuation fund, including investment fees, administration costs, insurance premiums, contribution fees and advisor fees. These fees and charges can be structured quite differently from product to product and can vary materially from product to product and advisor to advisor. As a rule of thumb, the greater the number of features of a product, the higher its rating will be; hence the greater the overall fee. In addition, a number of products offer fee discounts depending on an individual's fund balance and/or the buying power of the individual member's employer's fund.

A simplistic approach to assessing fees is therefore inappropriate. However, before selecting a superannuation product a full analysis of fees and charges needs to be undertaken so that you can ascertain which products represent best "value for money", taking into account your individual's personal circumstances and financial objectives. We therefore recommend that you seek advice from an appropriately qualified financial adviser.

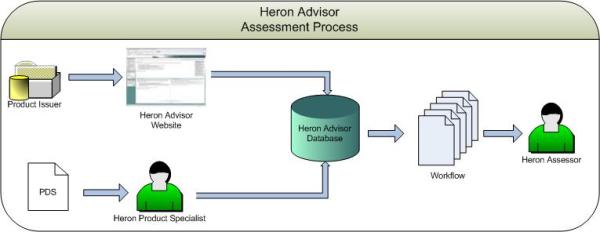

Heron Advisor is our purpose built system that we utilise to assess and store our product assessments. The following diagram explains how we keep our data continuously updated and current.

We have a number of methods in place to ensure that our data is always up to date:

As updated information is provided through any of these

methods, the changed information enters a workflow system which:

1. Notifies our assessment team of the change;

2. Allows them to review the change and reject it if the information

is not accurate or sufficient;

3. Provides a benchmark scoring guide specific to that product feature

which assists the assessor in determining an objective rating;

4. Prompts the assessor to update the Heron comments that may also

need changing as a result of the new information; and

5. Shows a comment to all users that the data has been altered, but

has not yet been reassessed for the time that the item remains in our

workflow log - ensuring complete transparency to all users reliant on

the data.

6. We also record details on the source data which includes the dates

of the last PDS materials, and names and dates of the product provider

that has verified the information in the data base.

Only after the assessor has approved and scored the change, is the information and scoring updated on the website.

The entire process is generally completed and the new data available on our website within 2 hours of receiving the updated information. As the data base is held on the web, there is no need for any product issuers to reload or refresh the database as we control this and it occurs instantaneously.